Over the last few months Berg Insight has been looking closely at the IoT platforms market.

There is a wide range of software platforms available, intended to reduce cost and development time for IoT solutions by offering standardised components that can be shared across many industry verticals to integrate devices, networks and applications. These third party IoT platforms are relatively new in the market and display a great diversity in terms of functionality. Broadly speaking, most IoT platforms fall into one of the following three categories: connectivity management platforms (CMPs), device management platforms (DMPs) and application enablement platforms (AEPs).

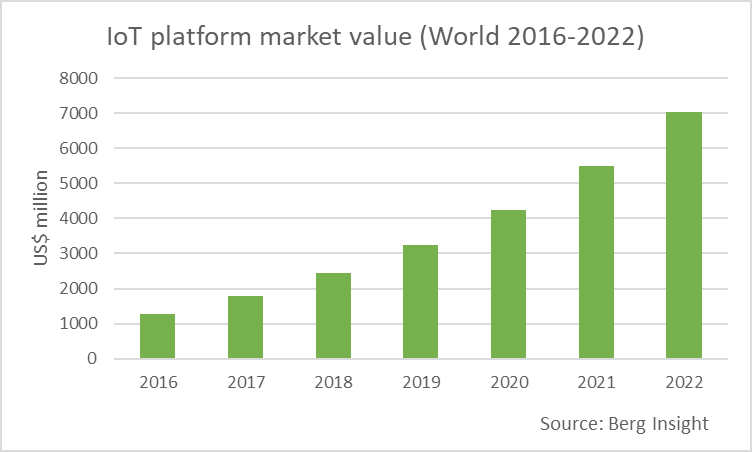

Berg Insight estimates that total revenues for third party IoT platforms will grow at a compound annual growth rate (CAGR) of 31.7 percent from € 1.78 billion in 2017 to € 7.05 billion in 2022.

The CMP market is characterised by a limited number of providers, although several new players have emerged in recent time following developments in the domains of LPWA and software-defined networks. Cisco Jasper is the dominant commercial CMP for mobile network operators worldwide and had about 75 million connections at the end of 2017. Other major vendors include Ericsson, Huawei, Amdocs, Comarch, as well as Nokia that launched its Nokia WING service in Q1-2017. Start-ups such as EMnify, Flo Live and Soracom have introduced cloud-based core networks dedicated for IoT that are offered as a service.

A number of major mobile operators continue to invest in the development of their proprietary platforms to differentiate from the competition. Vodafone’s Managed IoT Connectivity Platform stands out as the leading proprietary connectivity management platform with about 67 million connections at the end of 2017. CMPs are also a key component in the value proposition from IoT managed service providers. Aeris and KORE have consolidated their positions as leading players in this segment, with 10 million and 9 million connections respectively at the end of 2017.

The market for device management (DMP) and application enablement platforms (AEP) is notably crowded and has in recent time experienced a new wave of investments from major cloud infrastructure providers and enterprise software vendors. Leading providers of device management platforms include the major semiconductor IP supplier Arm, the cellular module manufacturers Sierra Wireless, Telit and Gemalto, as well as the independent software vendor Wind River.

The application enablement platform market is fragmented and populated by a host of start-ups, as well as major companies from the technology and industrial sectors. These companies have developed offerings that typically have a specific focus on a set of capabilities, often related to their core business. GE and PTC spearheaded the effort of promoting IoT in the industrial sector on a broader scale. While GE has shifted focus to mainly provide solutions rather than its Predix platform alone, PTC has emerged as the leader in the space.

Additional vendors with high involvement in the industrial sector include Software AG, Bosch, IBM, SAP, Oracle, Exosite, Device Insight and Altair Engineering. C3 IoT that specialises in data management and analytics has built a strong position in the utilities sector, followed by GE, Hitachi and IBM. Start-ups such as Ayla Networks, Arrayent (now part of Prodea), Greenwave Systems and Waylay have built substantial customer bases in the consumer electronics and smart home markets. Amazon, Google, Bosch and Samsung also serve large internal customers in this domain. An increasing number of companies target the transportation and smart cities markets including Bosch, Eurotech, Cisco, Davra, InterDigital, HPE and Nokia.