The 6th Annual Smart Energy UK & Europe 2015 may be a mouthful of a title, but it was worth mastering to understand the problems of rolling out smart energy metering across Europe, as Jeremy Cowan reports.

The London conference’s European stream opened in the expert hands of Constantina Filiou, principal administrator, Smart Grids at the European Commission (EC)’s Directorate General for Energy. Smart metering is being rolled out in the European Union (EU) “for the active participation of consumers,” she said. EU member states have already committed to roll-out 195 million smart meters for electricity and 45 million smart meters for gas by 2020.

Why? One reason is the potential for EU-wide cost and energy savings. A 2014 Commission report on the deployment of smart metering found that on average, smart meters provide annual savings of €160 for gas and €309 for electricity per metering point (distributed amongst consumers, suppliers, distribution system operators, etc.) as well as an average annual energy saving of 3%.

From the analysis of current national roll-out plans, the Joint Research Centre (JRC) at the Institute for Energy & Transport, together with the Directorate General for Energy, have estimated that almost 72% of European consumers will have a smart meter for electricity by 2020, through investments totalling €35 billion. (Also see: EC Institute for Energy & Transport.)

The EC’s 6 Benefits of Smart Metering

The European Commission has identified six ways in which smart metering will benefit consumers, through:

- Energy savings: Accurate & frequent consumption data

- Energy efficiency: Detailed consumption measurements

- Innovative services: Smart home solutions & home automation

- Consumer empowerment: Switching suppliers and modifying contract terms

- Sustainability: Renewable sources, storage potential in micro grids, and

- Distribution system efficiency: Cheaper, more effective management.

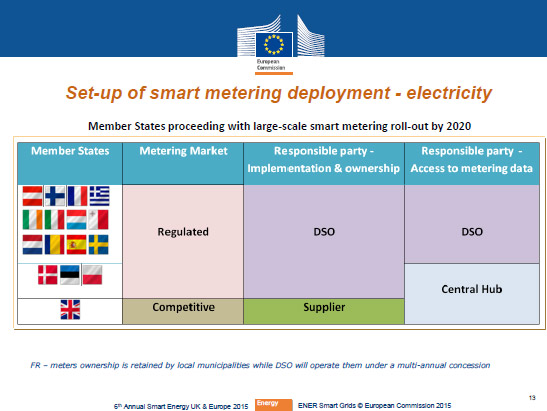

On satisfactory completion of each member state’s cost benefit analysis (CBA) the EC’s timetable then allows 10 years for implementation of widespread smart metering roll-out. An EC benchmarking report was adopted in June 2014 (prior to Croatia’s incorporation as the 28th EU member) under which 16 member states have shown widescale roll-out plans for smart metering by 2020. A further three states – Latvia, Slovakia and Germany — will be conducting only selective roll-outs.

Where costs outweigh benefits

Not all is rosey in the EU garden, though. Economic assessments of long-term cost benefits were to have been completed (where they were necessary) by September 2012. From that careful wording you will have deduced that this has not happened everywhere that it should.

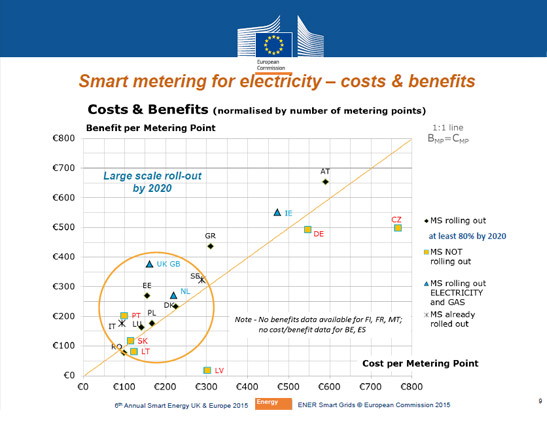

Why not? Well, the analyses show that roll-out costs vary enormously, from €77 to €766 per metering point, while the benefits per metering point range from just €18 to €654. Energy savings are gauged at anything from 0 to 5% per year, and the consumer benefits vary in Europe from 0.6% to 81%. The average smart meter lifetime is put at 15 years (+/- 4 years covers 56% of EU consumers).

Against such a wildly varied background it’s no wonder that the member states’ CBAs have led to different outcomes. In Germany, for example, the cost per metering point is almost €550 yet the benefit is below €500. Across the border in Austria, the cost is even higher at €590, but the reported benefit is more than €650 making large scale roll-out viable in Austria, where the German government says it is not. In addition, five states still have not provided the commission with adequate data; Belgium, Finland, France, Malta and Spain.

Only partial success so far

The EC is not saying so explicitly, but it’s hard to be impressed by the fact that only 16 of the 28 EU member states are on course to achieve widespread smart meter roll-out by the agreed date of 2020. And only eight of them will offer all the functions necessary to achieve the full benefits of metering.

Filiou told the London audience, “Smart meter functionalities should firstly be defined and set by national authorities prior to roll-out to benefit consumers; secondly, if they are not, they should at least be upgradeable; and lastly, they should be set up in accordance with international standards and EU Recommendation 2012/148/EU.”

As noted above, only eight countries roll-out plans (50% of large scale metering rollouts) consider all the recommended meter functionalities, says Filiou. The 10 common minimum smart meter functionalities are, according to the EC:

Consumer:

- Provide readings directly to the consumer and/or 3rd party

- Update readings frequently enough to use energy saving schemes

Metering operator:

- Allow remote reading by the operator

- Provide 2-way communication for maintenance and control

- Allow frequent enough readings for network planning

Commercial aspects of supply:

- Support advanced tariff system

- Remote ON/OFF control supply and/or flow or power limitation

Security – Data protection:

- Provide secure data communications

- Fraud prevention and detection

Distributed generation:

- Provide import/export and reactive metering.

(For more information on the EU’s smart meter roll-out programme see: Smart grids and meters.)

Recommendations

Clearly, some of the EU member states are making significant progress, with 195 million smart electricity meters and 45 million smart gas meters expected to be in operation by 2020, for approximately 72% of EU electricity consumers and 40% of gas consumers.

However, as Filiou points out, success is not just dependent on the scale of roll-out but also on the incorporation of all 10 functionalities. At present the European Commission is concerned that the planned roll-outs will benefit consumers less than they benefit Distribution System Operators (DSOs). “Success depends on criteria decided largely by (EU) member states,” says Filiou, such as, “smart metering functionalities, to include those benefitting also consumers, not just DSOs as owners/installers of meters. Retail market competition (will) breed innovative solutions and lower costs.”

Filiou concludes with six recommendations for the smart metering’s way forward.

- Understand the data handling options and the roles and responsibilities of market actors

- Build agreed data privacy & security frameworks

- Offer incentives for innovation and services

- Standardise meter functionalities

- Use information campaigns to build consumers’ trust and confidence

- Complete the member states’ Cost Benefit Analyses

For more information see:

The role of DSOs in a Smart Grid Environment

Comment on this article here or via Twitter: @jcm2m OR @m2mnow

![]()

![]()