In May 2020 Transforma Insights published the first iteration of its global IoT forecasts which predicted 24.1 billion connected devices generating US$1.5 trillion (€1.3 trillion) in 2030. However, the global picture belies a significant variation between regions. In particular, the vertical-specific opportunity is highly regionalised and growth in China will be driven by government policy more than organic adoption.

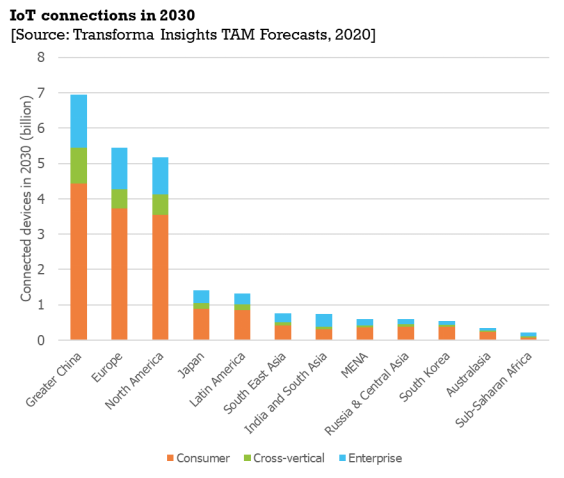

The global IoT market is dominated by three regions. Of the 24.1 billion connected IoT devices that Transforma Insights is predicting for 2030, the Greater China region (comprising China and Taiwan) is the largest with 6.9 billion. Europe is next with 5.5 billion and North America with 5.2 billion. The rest of the world has 6.6 billion.

To understand the regional dynamics better we need to dig into those numbers in more detail. Transforma Insights’ top level split of the market is between Consumer, Cross-Vertical (comprising generic devices used by businesses but which are not specific to the vertical, such as office printers or company fleet vehicles) and Enterprise (for devices which are specific to a particular vertical, such as smart grid for utilities or payment terminals for retail).

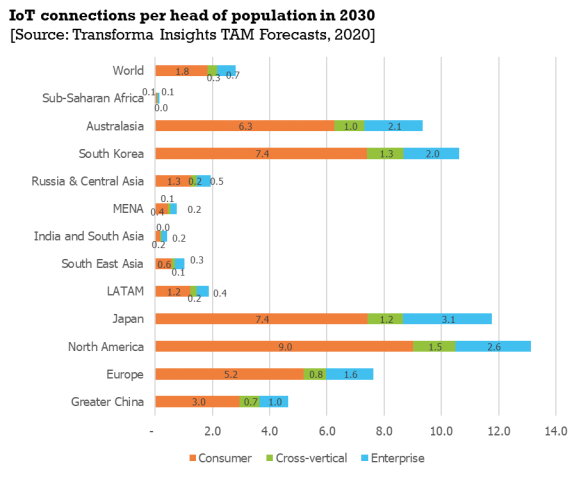

China’s lead over Europe and North America is largely due to the large volume of cross-vertical devices. This becomes more evident when we consider devices per head of population.

China has substantially lower Consumer devices per head: 3 per head versus 5.2 in Europe and 9 in North America. A similar picture emerges with Enterprise: 1 per head in China compared to 1.6 in Europe and 2.6 in North America. In contrast, China tracks much more closely in Cross-vertical devices: 0.7 versus 0.8 in Europe and 1.5 in North America.

In fact, considering also Japan, South Korea and Australasia, there is a relatively consistent proportion accounted for by Cross-vertical; much more so than the diverging Consumer and Enterprise sectors. The cross-vertical sector tends to include less sophisticated IoT use cases, driven in large part by the number of employees, businesses or households. Enterprise use cases tends to be much more specialised, and therefore unsurprisingly favours geographies that are more readily investing in process automation.

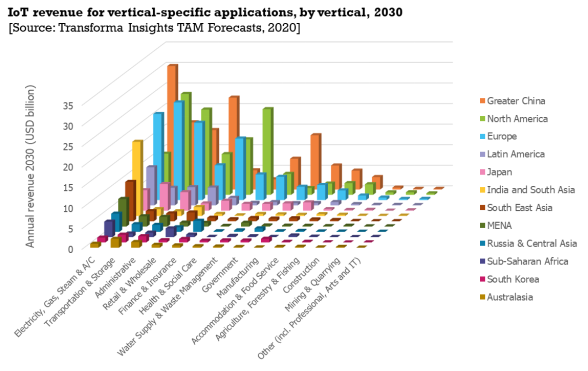

Delving further into the Enterprise category by looking at the revenue by vertical, it is notable that China, while still the biggest market, generally leads only in those segments that are driven by regulations, such as smart metre roll-outs in Electricity, Gas, Steam & A/C, and the Government category.

It lags Europe and North America to quite a significant extent in sectors such as Transportation & Storage, Administrative (which is dominated by building security and automation) and Finance & Insurance. Where the market is driven by the public sector, China is at the forefront, but where it depends on private sector investment, the vertical tends to lag. The one notable exception is Retail & Wholesale, where China seems to have embraced payment terminals and the cashless society in general leading to a higher adoption.

The other striking difference between the three major regions is the relative importance of Health & Social Care in North America. The US has long been the dominant market for IoT healthcare applications, reflecting a bigger and in many ways more nimble sector with greater emphasis on prevention.

Turning to the rest of the world, what we tend to find are highly populous markets such as India and South Asia, and South East Asia, being dominated by smart metre roll outs as the largest revenue generating sector. In more developed markets it tends to be more commercial sectors that dominate, such as Transportation & Storage, Finance and Manufacturing (the latter most notably in Japan and South Korea).

The key lesson from this brief dive into the forecasts is that there will be significant differences in the make-up of the adoption of IoT between regions in 2030. Not only that, but the market addressability is also quite regionalised. When Transforma Insights was compiling its geographical segmentation, it included significant consideration of uniqueness and replicability of solutions, i.e. how similar the economies are and how easily a solution might be transplanted from one geography to another.

Transplanting solutions between countries in Europe, North America or Latin America might be relatively simple. Less so in Asia. What emerges therefore is a picture of a diverse set of regions all with their own particular idiosyncrasies, offering different opportunities. A one-size-fits-all approach will not wash.

Comment on this article below or via Twitter: @IoTNow_OR @jcIoTnow