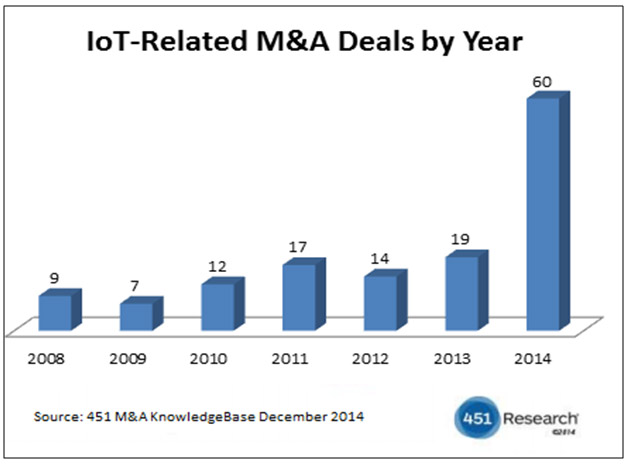

EXCLUSIVE REPORT: Internet of Things (IoT) deal-making activity rose sharply in 2014. Acquirers spent approximately $14.1bn to acquire 60 companies during the year. That spending sets a high watermark for the IoT industry and is nearly eight times the total spent by acquirers in all of the years prior to 2014.

The number of deals increased more than twofold from 2013 to 2014 as companies such as Google, Samsung, Cisco, Intel, PTC, Qualcomm and either staked out new ground or consolidated market position in IoT. 451 Research actively tracks IoT and wearable technology deal activity via its proprietary database, the 451 M&A KnowledgeBase, which records more than 40,000 technology merger and acquisition transaction since 2002.

451 Research formally defines the IoT as a system of networks, hardware, software and services enabling the objects of the physical world to become connected and communicate with other devices, applications or services through an information network (usually the Internet). Generally, the IoT market will have two related but application paths—consumer and industrial. The ultimate value of these systems will be tied to how effectively IoT data can be transformed into actionable insights—especially for industrial applications. There are innumerable processes that can be improved with IoT sensing, communications and control in nearly all major verticals, including consumer goods, transportation, utilities, military operations, healthcare delivery and product manufacturing. The expected benefits of IoT are improved system performance and efficiency, as well as creation of new sources of revenue and business models for IoT system buyers and sellers alike.

M&A activity so far in 2014 is almost evenly split between IoT-enabling horisontal infrastructure and vertical applications. In the infrastructure arena, acquirer’s notched 20 deals, primarily targeting a broad range of sensors, semiconductors, software platforms, security infrastructure and connectivity technologies needed for IoT to work effectively. Within the verticals, the transport and logistics segment led the field with 11 transactions so far this year, followed by the fitness and healthcare segment with 10 transactions. Acquirers also purchased five companies related to the home automation segment.

Key transactions identified by the 451 Research mobility team for the year include:

Home Automation and Control:

- Google acquired Nest Labs for $3.2bn in January.

- Nest Labs acquired Dropcam for $555m in June.

These deals were significant due to their size, revenue multiples, market valuation and the brands behind the transactions. Google and Samsung view the connected home as logical extensions from their respective positions of strength in smart devices and operating systems.

IoT-Enabling Platforms:

- PTC acquired Axeda for $190m in August. *

* This deal provides a lens into the changing competitive dynamics for making products smart. PCT’s IoT acquisition spree lines it up as a competitor to more traditional enterprise IT software players such as SAP, IBM and Oracle.

Semiconductors:

- Qualcomm Acquires CSR for $2.5b in October.

- Microchip Acquires ISSC for $328.5m in May.

Qualcomm and Microchip were both attracted to the products and expertise that their respective targets brought in low power Bluetooth wireless technologies.

The sharp rise in deal-making activity in 2014 suggests that market forces surrounding IoT have become compelling enough to call for action. As market forces align favorably around IoT in both consumer and industrial markets—solution providers want to cede nothing to the competition during the market’s developmental years. The understanding and acceptance of IoT will drive spending across a myriad of building-block categories from embedded computing systems to communication infrastructure, IP networking, platform, cloud, application and datacenter technologies that will form the foundation of the next generation of connected machines and services. We expect to see continued strong activity in 2015 as the cost and risk hurdles to IoT adoption are overcome and the competition to serve these markets increases. Any firm with the strategic intention of being an IT infrastructure and services leader over the next 10 years does not have the option to ignore this market.